Choosing between Creditsafe and D&B for business intelligence comes down to five questions:

Do you need credit risk data, sales prospecting data, or both?

Does your team require consistent international data across markets?

Are you willing to pay enterprise pricing for a bundled platform, or would you rather pick specialists for each function?

How important is speed of implementation versus depth of legacy coverage?

Do you need business data embedded in CRM and sales workflows, or is a standalone credit reporting tool enough?

In short, here's what we recommend:

Creditsafe fits credit and finance teams that need fast, affordable access to business credit reports and risk monitoring. Its database covers over 430 million companies across 200+ countries, and major credit insurers endorse its scorecard.

Creditsafe delivers the essentials of credit decisioning without the complexity or cost of a legacy provider, and it earns G2's top spot for fastest implementation and best ROI in its category. However, its data accuracy can be inconsistent for smaller or thinly-traded businesses, international scoring varies by country, and there's no self-serve pricing or purchase path.

D&B (Dun & Bradstreet) is the 185-year-old incumbent that covers credit risk and sales intelligence under one roof. Its D-U-N-S Number system spans 500M+ business entities globally and remains a requirement for government contracting and global trade finance. D&B also offers D&B Hoovers for sales prospecting and D&B Rev.Up ABX for account-based marketing.

But that breadth comes at a cost: enterprise-level pricing, a platform that users consistently call complex and hard to navigate, and a 2025 FTC settlement over misleading small businesses about its credit monitoring services.

Both platforms serve the credit and risk side of business intelligence well. But many teams comparing Creditsafe and D&B also need accurate contact data, buying signals, and sales automation. D&B bundles those into its offering through Hoovers, but the sales intelligence side consistently draws criticism for stale contact data and a difficult user experience.

For teams that need both credit intelligence and go-to-market data, there's a stronger approach than relying on D&B to do everything.

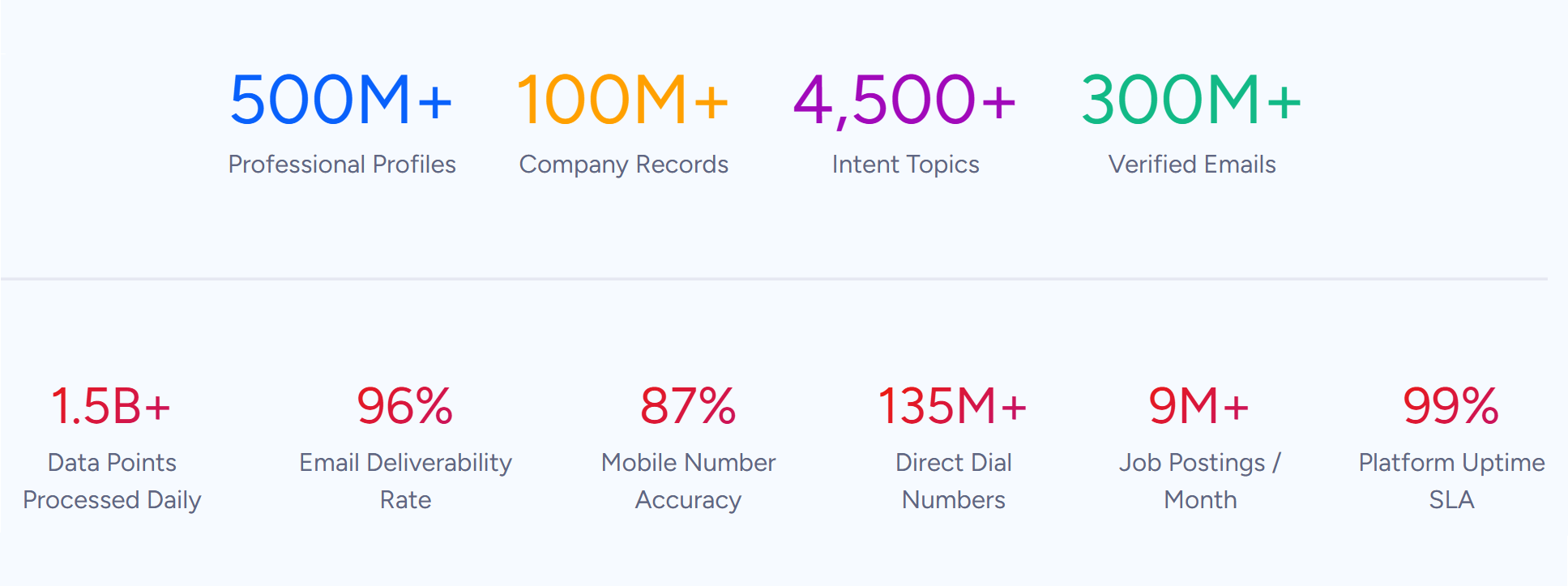

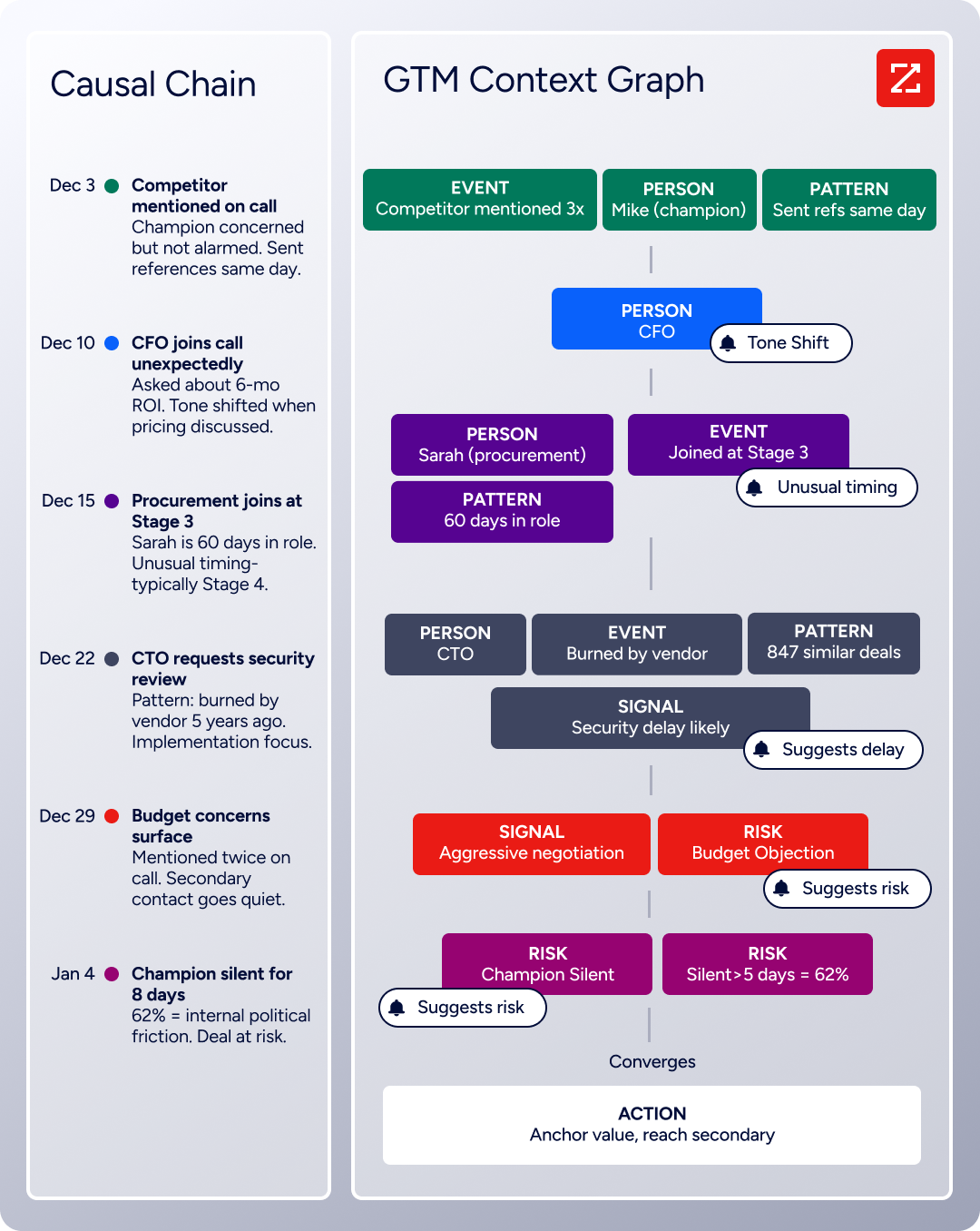

ZoomInfo is a GTM platform built on a B2B data foundation of 500M contacts, 100M companies, 135M+ verified phone numbers, and 200M+ verified business email addresses. Its GTM Context Graph processes 1.5B+ data points daily, combining this data with your CRM records, conversation intelligence, and behavioral signals to show not just what's happening in your deals, but why.

Sellers act on this intelligence through the GTM Workspace, marketers and RevOps teams build and launch plays from GTM Studio, and teams can power their own tools through ZoomInfo's Enterprise API and MCP server. For teams that need credit data alongside sales intelligence, pairing Creditsafe with ZoomInfo gives you the strongest tool for each function rather than settling for D&B's attempt to do both.

If combining dedicated credit intelligence with a GTM platform built for sales sounds right, see how ZoomInfo works.

Creditsafe vs. D&B vs. ZoomInfo at a glance

Creditsafe | D&B | ZoomInfo | |

|---|---|---|---|

Primary focus | Credit risk & compliance | Credit risk + sales intelligence | Sales intelligence & GTM |

Database size | 430M+ companies | 500M+ D-U-N-S records, 600M+ business records | 500M contacts, 100M companies |

Credit scoring | Proprietary 1-100 score, insurer-endorsed | PAYDEX, Failure Score, Viability Rating | N/A (pairs with credit tools) |

Contact data | Limited (officer data only) | 485M+ contacts via Hoovers (freshness issues) | 200M+ verified emails, 135M+ verified phones |

Intent & buying signals | None | Bombora add-on in Hoovers | Native intent, website visitor ID, signal stacking |

AI capabilities | Automated decisioning (Check and Decide) | D&B.AI suite, ChatD&B, SmartMail AI | GTM Context Graph, AI agents, GTM Workspace |

Pricing transparency | Custom/quote-based, no published prices | Enterprise pricing, Essentials from $49/mo | Custom-quoted, free tier available |

Best for | Credit teams needing affordable risk data | Enterprises needing D-U-N-S compliance | Revenue teams needing GTM intelligence |

Credit reporting is where these platforms diverge

Creditsafe and D&B both provide business credit reports, but their approaches reflect different philosophies.

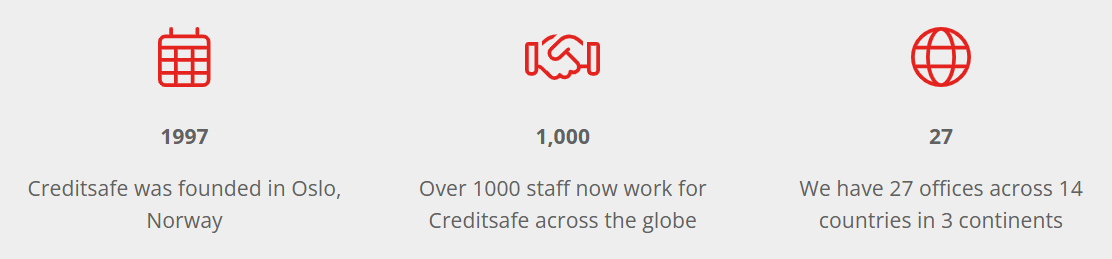

Creditsafe was founded in 1997 with one goal: deliver instant credit reports to small and mid-sized businesses at a fraction of what incumbents charged. That premise still shapes the product. Reports on 99.9% of companies arrive instantly online, and the platform is designed for non-financial staff to use without training.

Source: Creditsafe History

The credit scorecard predicts more than 70% of all business failures each month, drawing on financial ratios, industry analysis, trade payment data from 85 million tradelines, and public records.

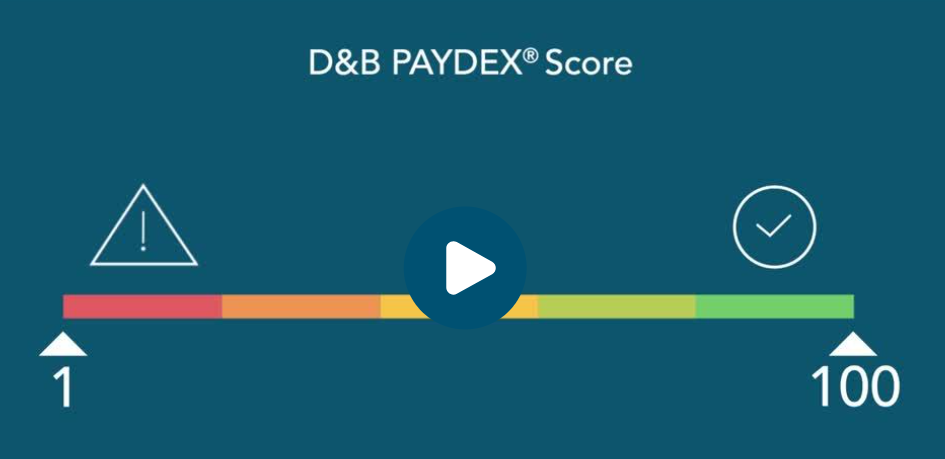

D&B brings 185 years of data accumulation. Its proprietary scores (the PAYDEX for trade payment behavior, the Failure Score for insolvency prediction, and the Viability Rating for business cessation probability) are embedded in corporate lending and procurement workflows worldwide.

Source: D&B PAYDEX

D&B Finance Analytics automates credit applications, portfolio monitoring, and account-level alerts. D&B ERAM centralizes global credit policies across 220+ countries for large enterprises.

The difference is accessibility versus depth. Creditsafe's credit reports give most teams what they need, quickly and affordably. D&B's credit infrastructure gives you more granular scoring and deeper corporate hierarchy mapping, but at enterprise pricing and with a steeper learning curve.

For companies that need the D-U-N-S Number for government contracting or regulatory compliance, D&B has no substitute. For everyone else, the question is whether D&B's additional depth justifies the cost.

Data coverage is wide on both sides, but accuracy varies

Both Creditsafe and D&B claim massive global databases.

Creditsafe covers 430 million companies across 200+ countries, sourced from over 9,000 data sources, and updated over 1 million times per day. D&B's Data Cloud covers more than 600 million businesses across 200+ countries.

Source: Creditsafe Data

But raw numbers don't capture the user experience.

Creditsafe's weaknesses show up with smaller, thinly-traded businesses. G2 reviewers note that companies without reported trade lines receive benchmark scores of limited value, and that the scoring logic for these businesses often seems thin.

Entity resolution is another problem: companies sometimes appear under different addresses or names, making it hard to confirm you're looking at the correct legal entity.

D&B faces accuracy issues in different areas. Outdated contact data is the most common complaint across G2 and Capterra reviews. Contacts who have left companies or retired still appear in search results and consume credits. International data quality drops sharply outside North America, particularly for smaller private companies.

Creditsafe acknowledges similar international limitations, noting that data availability varies by country due to local filing requirements and regulations.

For company-level financial data and credit scoring, both platforms are credible in their core markets. But for contact-level data (names, emails, phone numbers, job titles), neither Creditsafe nor D&B is built for the task.

That's where ZoomInfo fills a gap neither credit platform was designed to address.

Source: ZoomInfo

Sales intelligence separates a credit tool from a GTM platform

This is where the comparison between Creditsafe and D&B breaks open, because D&B tries to be both a credit platform and a sales intelligence platform. Creditsafe does not.

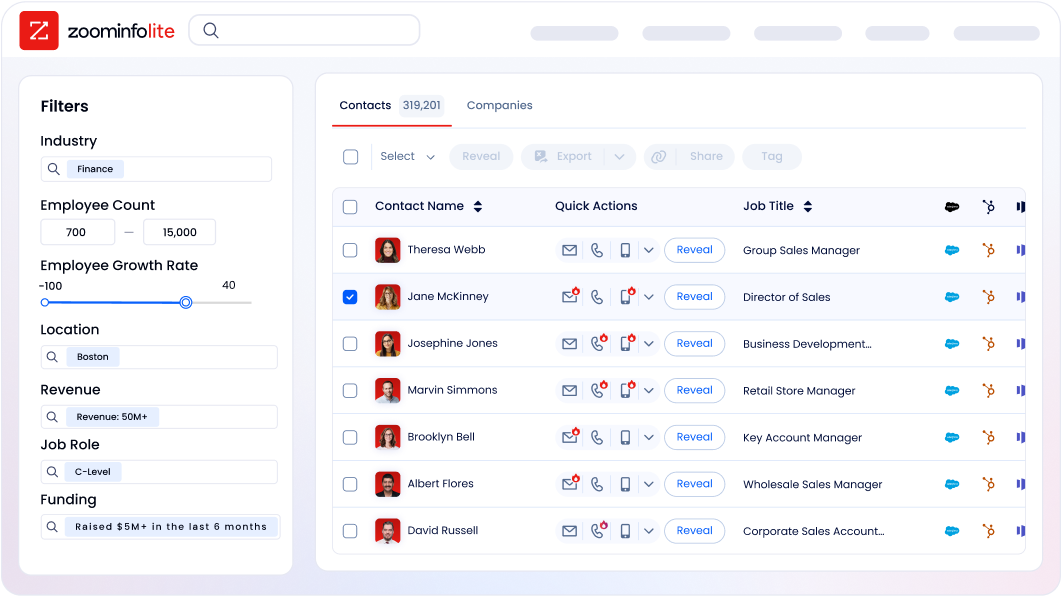

D&B Hoovers offers access to more than 330 million companies and 485 million+ contacts with more than 200 search filters. Recent AI additions include SmartSearch AI for natural-language list building and SmartMail AI for automated outreach in 19 languages. On paper, it sounds comprehensive.

Source: D&B Search

In practice, users report consistent problems. G2 reviewers describe a platform with too many clicks to reach the information they need and a cluttered filtering system. Capterra reviewers flag a record export cap of 1,000 records per action and contact data that is frequently outdated.

The dual-credit consumption model means each prospect uses two credits (one company + one contact), making the true cost per usable record hard to predict when many contacts are stale.

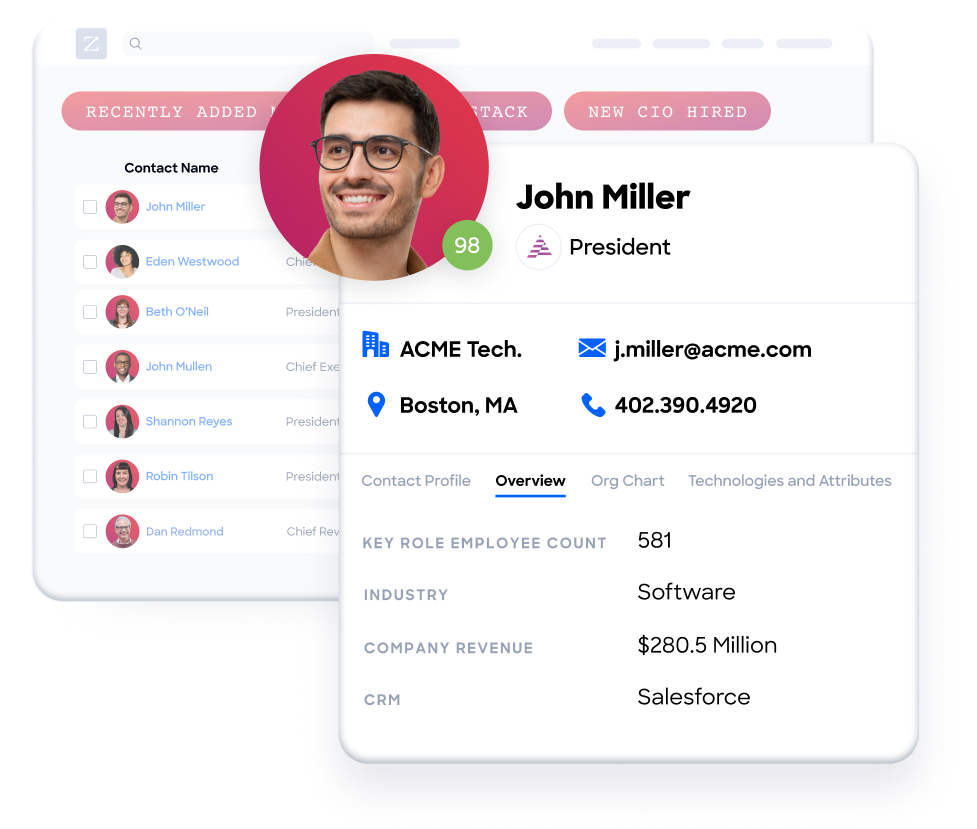

ZoomInfo was built from the ground up for this problem. Its database of 500M contacts, 135M+ verified phone numbers, and 200M+ verified business email addresses is maintained through a multi-source verification pipeline backed by 300+ human researchers, achieving up to 95% accuracy on first-party data.

Source: ZoomInfo Data

In a Fortune 500 competitive RFP analyzing 25 million contacts across vendors, an independent consultant concluded that "no other competitor came even close."

Beyond contact data, ZoomInfo provides capabilities that D&B Hoovers doesn't match. Buyer Intent data tracks signals from 210 million IP-to-Organization pairings and 6 trillion+ keyword-to-device pairings monthly, showing which companies are actively researching solutions in your category.

WebSights resolves anonymous website traffic to specific companies and buying team members. Technographics profile the tech stacks of 30+ million companies across 30,000+ technologies.

Source: ZoomInfo WebSights

D&B Hoovers offers Bombora intent data as an add-on and a Visitor Intelligence add-on, but these are bolted onto a platform whose core strength is company-level financial data, not contact-level sales intelligence. D&B's Niche Player placement in the 2024 Gartner Magic Quadrant for Account-Based Marketing Platforms reflects this gap.

ZoomInfo was named a Leader in the same Magic Quadrant for the second consecutive year and holds 133 No. 1 rankings on G2 across Sales Intelligence, Buyer Intent, Data Quality, and related categories.

Seismic attributed 39% of active pipeline to opportunities identified or influenced by ZoomInfo signals, with a 54% productivity gain across the sales team. (Seismic Case Study)

The D-U-N-S Number is D&B's structural moat

If your business requires the D-U-N-S Number for government contracts, regulatory compliance, or trade finance, this section ends the comparison. D&B's D-U-N-S Number, introduced in 1963, is a nine-digit unique business identifier covering 500M+ entities and trusted by over 90% of Fortune 500 companies.

Source: D&B's D-U-N-S Number

No competitor offers an equivalent. If a regulatory body, government contract, or supply chain partner requires D-U-N-S verification, you need D&B.

This identifier also powers D&B's corporate hierarchy mapping, linking parent companies, subsidiaries, and branches across global operations. For credit teams managing group-level exposure across multi-entity organizations, this corporate linkage data is a real advantage over Creditsafe's more limited group structure coverage.

But the D-U-N-S Number is a compliance requirement, not a reason to consolidate all your business data needs onto D&B's platform. Many enterprises use D&B for D-U-N-S compliance and credit risk data while sourcing sales intelligence from a dedicated platform.

Compliance and KYC take different approaches

Both Creditsafe and D&B have expanded beyond credit reports into compliance screening, reflecting the growing overlap between credit risk and regulatory due diligence.

Creditsafe's compliance suite centers on Creditsafe Protect, which screens against PEP databases, sanctions lists, and adverse media using over 35,000 official sources and the LexisNexis WorldCompliance database with 4.8 million profiles across 50+ risk categories.

Source: Creditsafe Protect

A key strength: Creditsafe automatically identifies directors, shareholders, and Ultimate Beneficial Owners from its company database, cutting manual entry. The platform also claims a 50-80% reduction in false positives. Because compliance and credit data share the same platform, a user can go from a company search to a final compliance decision in one system.

D&B's compliance offering, D&B Compliance Intelligence, was named a category leader by Chartis Research in the 2025 RiskTech Quadrant for KYC Data, specifically for corporate hierarchies and trade intelligence.

Source: D&B Compliance Intelligence

The compliance suite uses Dow Jones-integrated data for sanctions and watchlist screening, covers 600M+ entities and 400M+ shareholders globally, and includes a configurable risk engine for automated KYC/KYB classification. D&B's May 2026 partnership with Anthropic specifically targets automating KYC/KYB workflows for banks and FinTechs.

For teams that handle both compliance screening and sales outreach, there's an important distinction. Creditsafe and D&B both integrate compliance with credit data. Neither integrates compliance with verified contact data for sales follow-up.

ZoomInfo's database provides the contact-level intelligence (verified emails, direct dials, org charts) that lets sales teams act on compliance-cleared accounts immediately, rather than manually sourcing contact information after screening.

AI capabilities reflect each platform's priorities

All three platforms have invested in AI, but in different directions.

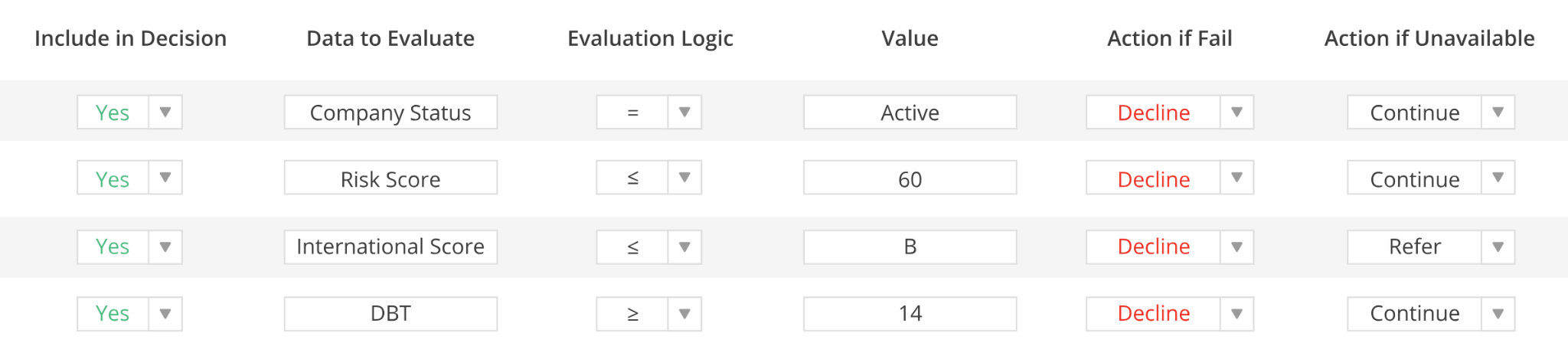

Creditsafe's AI focuses on automated credit decisioning. Check and Decide is a no-code decision engine that replaces manual credit review workflows with rules-based approvals, running decisions in real time against Creditsafe's database. Most customers go live in under three days. This is practical AI: it automates a specific workflow (credit approvals) rather than promising broad intelligence.

Source: Creditsafe Check & Decide

D&B launched D&B.AI in October 2025, a suite that includes ChatD&B (a conversational interface to D&B's data), AI agents for credit risk and supplier evaluation, and MCP servers for feeding D&B data into third-party AI agents. SmartSearch AI and SmartMail AI were added to D&B Hoovers in August 2024.

The AI ambition is broad, but it's early. D&B's core data strength is at the company entity level, and the AI features sit on top of a platform that users already find complex.

ZoomInfo's AI operates on a different foundation. The GTM Context Graph processes 1.5B + data points daily, combining ZoomInfo's B2B data with customer CRM records, conversation intelligence from Chorus (which captures every call and meeting), and behavioral signals.

Source: ZoomInfo Context Graph

The result: an intelligence layer that captures not just what happened in a deal, but why. GTM Workspace gives sellers AI agents that handle account research, outreach drafting, signal monitoring, and CRM updates. GTM Studio lets marketers and RevOps teams build audiences in natural language and launch multi-channel plays without engineering support.

Source: ZoomInfo GTM Workspace

The difference: Creditsafe's AI automates credit decisions. D&B's AI aims to make its data more accessible. ZoomInfo's AI connects signals to outcomes across your entire go-to-market operation.

"ZoomInfo's built a full system of execution. GTM Intelligence works the list, writes the outreach, triggers the play, and helps drive predictable growth." — Ian Brodie, CEO & Co-Founder, Levanta (Levanta Case Study)

Pricing models reflect different market positions

Pricing transparency is a weakness across all three platforms, but the structures differ.

Creditsafe publishes no dollar figures. The US pricing page states that "pricing is shaped around your business" and leads to a "Request Quote" form. Three credit reporting tiers (Standard, Plus, Premier) offer escalating allowances: from 5 international credit reports and 100 monitored US companies at the entry level, to 150 international reports and unlimited US monitoring at Premier.

The Connect API, automated decisioning, and compliance products are sold as separate packages. Contracts default to 12 months with no self-serve cancellation. Buyer testimonials cite cost advantage over competitors as a consistent selection driver.

D&B operates two models. The self-serve D&B Hoovers Essentials starts at $49/month for 150 company credits and 150 contact credits, but the dual-credit system means each prospect uses two credits, effectively supporting 150 prospects per month. Standalone credit reports are sold in packs: a single Business Information Report costs $189.99, with volume discounts up to 20% off at 25 packs.

Enterprise pricing for D&B Hoovers, Finance Analytics, and other products is not publicly disclosed. Auto-renewal is explicitly at the "List Price in effect at the time of renewal, which may be higher than today's price," and the 2025 FTC settlement involved allegations of enrolling customers in auto-renewal contracts without clear disclosure.

ZoomInfo uses a custom-quoted, seat-and-credit-based subscription model with three product lines (Sales, Marketing, and standalone products like Chorus and Chat). There are no published prices for paid tiers.

However, ZoomInfo offers something neither Creditsafe nor D&B provides: a permanent free tier called ZoomInfo Lite with access to the B2B database, 10 monthly export credits, search and filtering, a Chrome extension, and website visitor identification. A separate 7-day free trial provides access to the full platform.

Source: ZoomInfo Lite

Note: ZoomInfo is transitioning toward a consumption-based pricing model.

The pricing reality: if you only need credit reports and monitoring, Creditsafe will likely cost less than D&B for comparable functionality. If you need both credit data and sales intelligence, paying separately for Creditsafe (credit) and ZoomInfo (GTM) may offer better value than D&B's bundled enterprise pricing, since you'd get the strongest tool for each function rather than a compromise on the sales intelligence side.

Integrations determine whether data reaches your workflows

Creditsafe integrates natively with major CRM and ERP platforms including Salesforce, Sage 50/200, NetSuite, Microsoft Dynamics, SAP, SugarCRM, and HighRadius. Its Connect API provides RESTful access to the full database with JWT authentication. The Salesforce BI Plus App automatically enriches records with 32 fields and refreshes data every 14 days.

Source: Creditsafe with Salesforce

For credit teams embedded in accounting and ERP workflows, Creditsafe's integration footprint is practical and well-targeted.

D&B integrates with Salesforce, Oracle, and SAP at the enterprise level. The D&B Direct 2.0 API provides access to 600M+ businesses through both REST and SOAP architectures. D&B Hoovers connects to Salesforce, Microsoft Dynamics 365, and HubSpot. D&B's newer MCP servers deliver data to AI agents.

The integration ecosystem is broad but reflects D&B's fragmented product suite; different products have different integration depths.

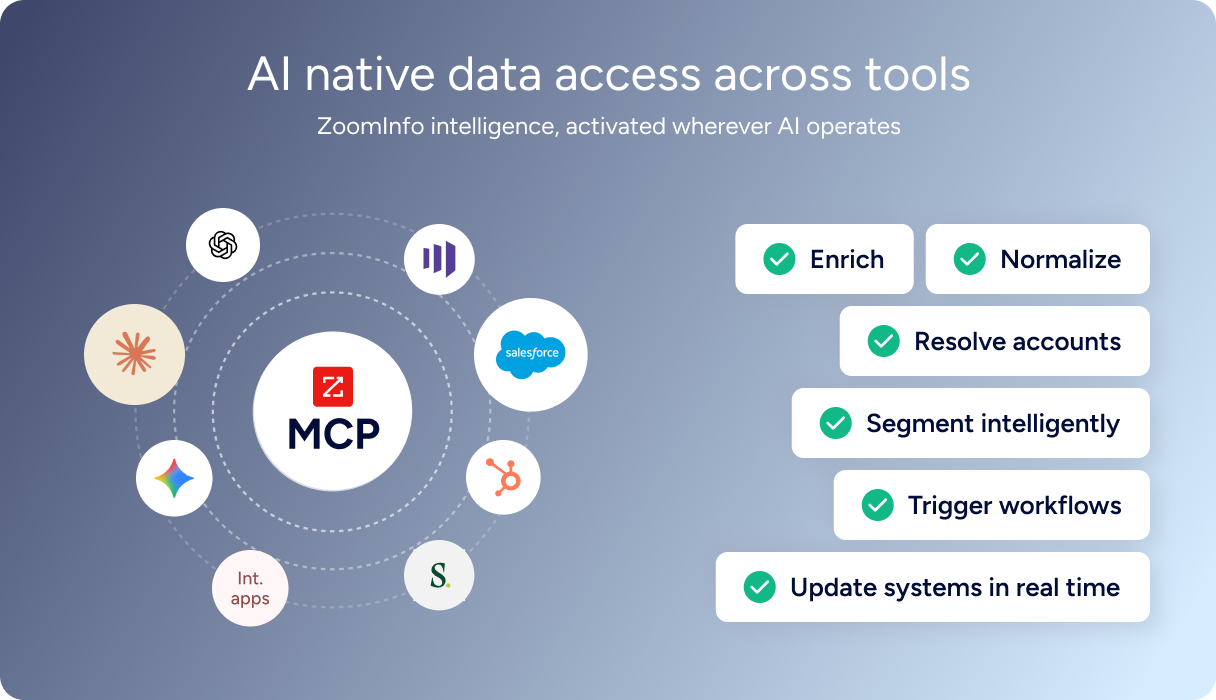

ZoomInfo takes integration further. The ZoomInfo App Marketplace lists 120 partner integrations across CRM, marketing automation, sales engagement, revenue intelligence, and data warehouse categories.

The Enterprise API provides programmatic access with OAuth 2.0 authentication, covering search, enrichment, AI intelligence (via the Copilot API), and marketing audience management. API access is included in all relevant plans.

Source: ZoomInfo API

The ZoomInfo MCP server connects AI models directly to ZoomInfo's data as a native tool, currently supporting Claude and ChatGPT. Cloud Partners enable direct data ingestion into AWS, Google Cloud, Snowflake, and Databricks.

Source: ZoomInfo MCP

The key difference: Creditsafe integrates credit data into finance workflows. D&B integrates company data into both finance and sales workflows (with varying depth). ZoomInfo integrates contact data, buying signals, and AI intelligence into every surface where go-to-market decisions happen, from CRM to custom AI agents.

"The plug-and-play aspect of the API means I can integrate it into any process and get information at a moment's notice." — Jerry Wilson, Senior Marketing Intelligence Analyst, BDO Canada, which achieved an 87% reduction in time spent on data dashboard updates. (BDO Canada Case Study)

Monitoring and alerting serve different objectives

Creditsafe's Company Monitoring covers 49 countries with 20+ alert types: credit score changes, director changes, legal notices, payment behavior shifts. Alerts fire the moment an event occurs, turning portfolio risk management from a periodic manual review into a continuous automated process.

Source: Creditsafe Company Monitoring

The Trade Payment Program adds a behavioral incentive: enrolled companies pay faster when they know their payment behavior is tracked and reported.

D&B's monitoring is distributed across products. D&B Finance Analytics Account Manager runs continuous monitoring for PAYDEX changes, derogatory filings, and financial events. D&B Hoovers offers Trigger Alerts for M&A announcements, executive changes, and contract wins.

D&B Supplier Intelligence monitors supply chain risk with sanctions screening and location analysis. The depth is real, but accessing these alerts requires navigating separate products with separate interfaces.

Source: D&B Supplier Intelligence

ZoomInfo's monitoring is oriented around sales opportunities, not credit events. Buyer Intent surfaces companies actively researching solutions. WebSights identifies anonymous website visitors. GTM Workspace's Action Feed streams real-time buying signals (G2 comparisons, funding events, executive hires) matched to target criteria, with pre-drafted actions on every signal.

Source: ZoomInfo Intent Data

For sales teams, these signals drive pipeline. For credit teams, Creditsafe or D&B monitoring remains essential.

The practical takeaway: if you're monitoring for credit risk, Creditsafe's alerting system or D&B's Finance Analytics are the right tools. If you're monitoring for sales opportunities, ZoomInfo's signal infrastructure is well ahead of what either credit platform offers.

Creditsafe vs. D&B vs. ZoomInfo: Which should you choose?

The right choice depends on which business functions need the data.

Choose Creditsafe if:

Credit risk management is your primary need

You want fast implementation and an interface non-financial staff can use

You need affordable credit reports with strong monitoring and compliance

Your team handles credit decisions, supplier vetting, and AR management

You don't need the D-U-N-S Number for regulatory compliance

Choose D&B if:

The D-U-N-S Number is a regulatory or contractual requirement

You need enterprise-grade credit infrastructure across 220+ countries

You're already embedded in the SAP, Oracle, or Salesforce enterprise ecosystem

Your organization needs both credit risk and sales intelligence in one contract

You have the budget and onboarding capacity for a complex enterprise platform

Choose ZoomInfo (alongside your credit platform) if:

Your sales team needs verified contact data, direct dials, and buying signals

You want AI that reasons across your deals, not just looks up company records

You need to activate data in CRM, marketing automation, and custom AI agents

You're building an outbound sales motion or account-based marketing program

You want the best tool for each job: credit specialist + GTM specialist

Start with ZoomInfo Lite for free or request a demo of the full platform.

The deeper insight: D&B's attempt to span both credit risk and sales intelligence means it competes with Creditsafe on one side and ZoomInfo on the other, without clearly winning either contest. Creditsafe offers faster, more affordable credit intelligence. ZoomInfo offers stronger sales intelligence with AI that drives revenue.

For teams that need both, pairing the right specialist for each function gives you stronger capabilities at each layer than any single platform trying to do everything.

"You'll get 10x the value if you think of ZoomInfo as a full platform and not just a tool for one team." — John Kotsuros, Founder and CEO of SpringDB, which saw 2x-3x increases in campaign conversions after enriching data with ZoomInfo. (SpringDB Case Study)

Creditsafe vs. D&B vs. ZoomInfo FAQ

What is the core difference between Creditsafe, D&B, and ZoomInfo?

Creditsafe is a business credit intelligence platform focused on credit reports, risk scoring, compliance screening, and collections for B2B finance teams. D&B is a 185-year-old data and analytics provider that spans both credit risk (Finance Analytics, ERAM, Compliance Intelligence) and sales intelligence (D&B Hoovers, Rev.Up ABX, Connect).

ZoomInfo is a GTM platform built for sales, marketing, and revenue operations, with 500M contacts, buyer intent signals, and AI agents that automate prospecting and deal execution.

Which platform has better data coverage?

All three cover 200+ countries. Creditsafe tracks 430 million companies with 85 million trade payment tradelines. D&B covers 600 million+ business records and 500 million+ D-U-N-S Numbers. ZoomInfo covers 500 million contacts, 100 million companies, and 135 million+ verified phone numbers.

The key distinction is data type: Creditsafe and D&B specialize in company-level financial and risk data, while ZoomInfo specializes in contact-level data verified for sales outreach with up to 95% accuracy on first-party data.

Is the D-U-N-S Number required, and can I get it without using D&B for everything?

The D-U-N-S Number is required for US government contracting, many global trade finance processes, and procurement workflows at large enterprises. It is exclusive to D&B (no other provider offers it). However, you can use D&B for D-U-N-S compliance and credit risk while sourcing sales intelligence from a dedicated platform like ZoomInfo.

How does pricing compare for credit reports specifically?

Creditsafe does not publish prices but offers tiered subscription packages with unlimited US credit report access included in paid tiers. D&B sells individual Business Information Reports at $189.99 each, with volume discounts up to 20% on 25-packs.

D&B Hoovers Essentials starts at $49/month but is a sales prospecting tool, not a credit reporting package. Enterprise pricing for both platforms requires contacting sales.

Which platform is best for sales prospecting and outreach?

ZoomInfo is the stronger choice for sales intelligence. It holds 133 No. 1 rankings on G2 across Sales Intelligence and related categories and was named a Leader in the Gartner Magic Quadrant for ABM Platforms for two consecutive years.

D&B Hoovers provides sales prospecting capabilities but was placed as a Niche Player in the same Gartner Magic Quadrant, and users consistently report outdated contact data and a difficult interface. Creditsafe does not offer sales prospecting features.

Can I use Creditsafe or ZoomInfo alongside D&B?

Yes. Many enterprises use D&B for D-U-N-S compliance and credit scoring while pairing it with Creditsafe for more affordable day-to-day credit monitoring or with ZoomInfo for sales intelligence and GTM execution. ZoomInfo integrates with Salesforce, HubSpot, Microsoft Dynamics, and 120+ other tools, making it straightforward to combine with any credit data platform.

Which platform has the strongest AI capabilities?

Creditsafe's AI focuses on automated credit decisioning through its Check and Decide engine, which most customers deploy in under three days. D&B launched D&B.AI in October 2025 with ChatD&B, AI agents, and MCP servers for AI integration.

ZoomInfo's GTM Context Graph processes 1.5 billion+ data points daily, combining B2B data with CRM records, conversation intelligence from Chorus, and behavioral signals. ZoomInfo's AI agents in GTM Workspace handle account research, outreach drafting, and signal monitoring, and the platform was named a Leader in the Forrester Wave for Intent Data Providers in Q1 2025.

What about the FTC action against D&B?

In September 2025, D&B agreed to pay $5.7 million to settle FTC allegations that it misled small and mid-sized businesses about its credit monitoring services, including overstating risk to pressure purchases and enrolling customers in auto-renewal contracts without clear disclosure. D&B must now maintain a third-party quality monitor and certify annual compliance.

Neither Creditsafe nor ZoomInfo has faced comparable regulatory action.